Hyperliquid Strategies has built its treasury around HYPE, but its first SEC filings show the strategy already faces a fundamental challenge.

The company wants to accumulate more tokens for shareholders while warning investors it may need to sell HYPE into future capital raises, placing long-term accumulation goals alongside the practical limits of market liquidity.

Hyperliquid Strategies says the primary objective to accumulate HYPE tokens on behalf of stockholders will be funded by proceeds from its Closing PIPE and future capital raises.

The company established a committed equity facility with Chardan that allows it to direct up to $1 billion in common stock sales, with the company controlling the timing of those sales.

The PIPE package that seeded the strategy included about $299.9 million in cash and 12,517,592 HYPE tokens valued at $580.5 million at signing, for an aggregate fair value of $880.4 million before costs.

By closing, those same HYPE tokens were worth $411.3 million, a $169.2 million loss on the contribution before the company bought a single additional token.

As of May 14, Hyperliquid Strategies held about 20.8 million HYPE, which it said was the largest HYPE position of any US public company.

The filing carries a warning that, during periods of market instability, the company might sell HYPE at unfavorable prices.

| Item | Figure | Why it matters |

|---|---|---|

| Strategic objective | Accumulate HYPE for stockholders | Turns HYPE into a public-company treasury asset |

| Equity facility | Up to $1.0B in common stock sales | Gives the company a repeatable capital-raising path |

| PIPE cash | $299.9M | Immediate buying capacity |

| HYPE contributed at signing | 12.52M HYPE valued at $580.5M | Seeded the treasury strategy with direct token exposure |

| HYPE value at closing | $411.3M | Shows mark-to-market risk before new accumulation |

| Contribution loss | $169.2M | Demonstrates how fast token volatility can hit the wrapper |

| HYPE held as of May 14 | 20.8M HYPE | Baseline for future accumulation or dilution analysis |

A second wrapper waiting on approval

Grayscale filed a preliminary prospectus for a proposed Hyperliquid Staking ETF, formerly known as “Grayscale HYPE ETF,” on May 26.

The document itself states that the trust may not sell its securities until the registration statement takes effect, meaning the product currently exists only on paper.

The trust would hold HYPE directly and aim to reflect HYPE’s per-share value, including staking rewards if the fund implements staking. The filing says staking takes about 24 hours and unstaking about 7 days, depending on demand.

That window would sit between the trust and its staked HYPE liquidity during the kind of market stress when share creation, redemption, and hedging mechanics matter most.

Hyperliquid’s validator count is 33 as of June 9, and Grayscale’s filing warns that a set that small could coordinate to influence transaction ordering, market parameters, listing and delisting decisions, and governance itself.

The filing backs that warning with two incidents already on the record. In March 2025, an attacker inflated the JellyJelly token’s price by 429%, HLP losses reached $12 million, and validators delisted the token and settled positions in about two minutes.

In November 2025, a POPCAT manipulation incident produced an estimated $4.9 million in losses, and Hyperliquid halted withdrawals during the response.

The filing presents both incidents as examples of how quickly validators and protocol operators can coordinate during market stress, while warning that the same speed can deepen centralization concerns.

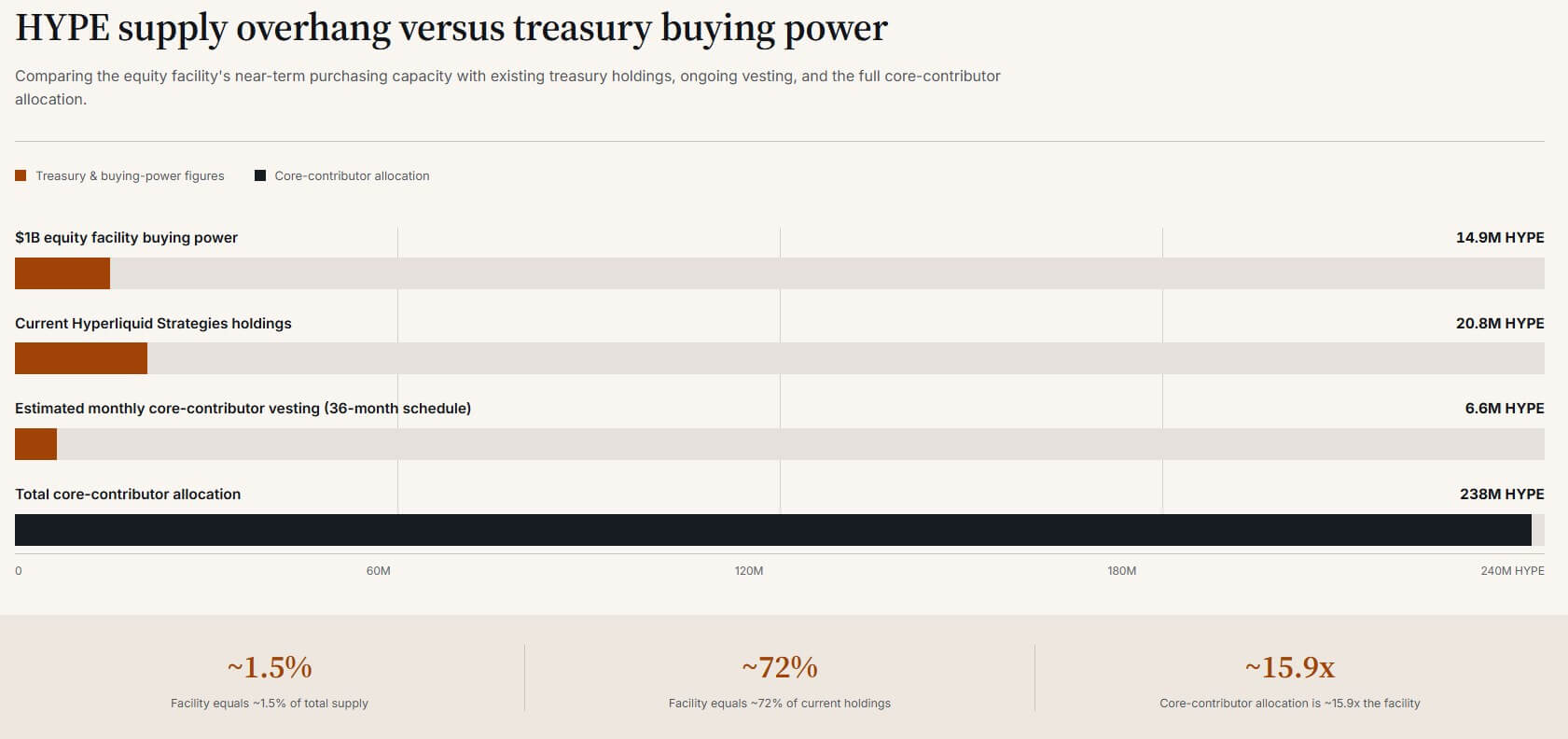

The supply overhang behind the buying

The protocol caps HYPE’s total supply at 1 billion tokens, with 310 million already distributed and unlocked through Genesis, 238 million held by core contributors, vesting monthly from November 2025 through 2027 and 2028, and a further 388 million reserved for future emissions and community rewards.

That 238 million core contributor allocation is worth about $15.9 billion at a HYPE price near $67, roughly 15.9 times the size of the $1 billion facility Hyperliquid Strategies can draw on to buy HYPE.

A fully used facility would add about 14.9 million tokens to the company’s holdings, just under 1.5% of the total supply and about 72% of its current position.

Spreading the core contributor unlock across 36 months puts monthly vesting near 6.6 million HYPE, worth roughly $443 million at today’s price, a monthly figure equal to about 44% of the entire $1 billion facility’s total buying power.

At the time of writing, DefiLlama tracked Hyperliquid with nearly $10.4 billion in open interest against a $14.9 billion HYPE market cap, putting open interest at about 70% of the token’s market cap.

The 30-day perpetual volume runs $210.1 billion, over 20 times open interest, and 30-day liquidation volume totals $2.6 billion, about 25% of open interest on its own.

Those numbers describe a venue that runs on constant margin and constant liquidation, the environment that both the treasury filing and the ETF prospectus flag as the place HYPE’s saleability gets tested.

What the next few months could decide

A bull path has Hyperliquid Strategies raising stock at favorable levels relative to its net asset value, staking yield making HYPE exposure stickier for holders, and HYPE’s market cap expanding fast as liquidation volume shrinks as a share of open interest.

If Grayscale’s proposed fund launches, its premiums and discounts stay tight, and HYPE starts trading like a credible public-market treasury asset with a value story beyond its perp venue.

A bear path has HYPE’s price falling as open interest and liquidations climb, pushing Hyperliquid Strategies’ shares below their net asset value and making further stock issuance more dilutive.

Spot liquidity would be thin enough to strain authorized-participant hedging, spreads would widen around any proposed fund, and HYPE spot volume would fall short of the scale needed to absorb monthly vesting without moving the price.

Public market access would then amplify the token’s volatility, the risk these wrappers promise to reduce.

| Metric to watch | Bull path | Bear path | Why it matters |

|---|---|---|---|

| Hyperliquid Strategies stock vs NAV | Trades at premium or near NAV | Trades below NAV | Determines whether equity issuance is accretive or dilutive |

| HYPE market cap vs open interest | Market cap grows faster than OI | OI stays high while market cap falls | Shows whether venue leverage is becoming more or less dangerous |

| 30-day liquidation volume / OI | Falls below current ~25% level | Climbs above current level | Measures stress inside the perp venue |

| ETF premium/discount, if launched | Tight spreads | Persistent discount or wide spreads | Tests whether the wrapper can track HYPE in volatile conditions |

| AP and market-maker hedging | Orderly liquidity | Hedging friction and wider spreads | Key risk in the Grayscale filing |

| Monthly vesting absorption | Spot demand absorbs unlocks | Vesting overwhelms spot liquidity | Tests whether treasury/ETF demand can offset supply pressure |

| Validator interventions | No emergency coordination | New delisting, halt, or bridge incident | Determines whether “protective coordination” becomes centralization risk |

Hyperliquid’s validator interventions in JellyJelly and POPCAT read as protective just as easily as they read as centralized, and the record so far supports both readings.

A treasury company and a proposed staking ETF are both offering public market access to a token whose own paperwork admits it might not be sellable at the moment access counts most.