A UBS tokenized money-market fund is now being used as live collateral on Bybit, turning one of Wall Street’s RWA products into working exchange margin. The milestone gives yield-bearing collateral a real trading use case, while leaving the most important risk terms out of public view.

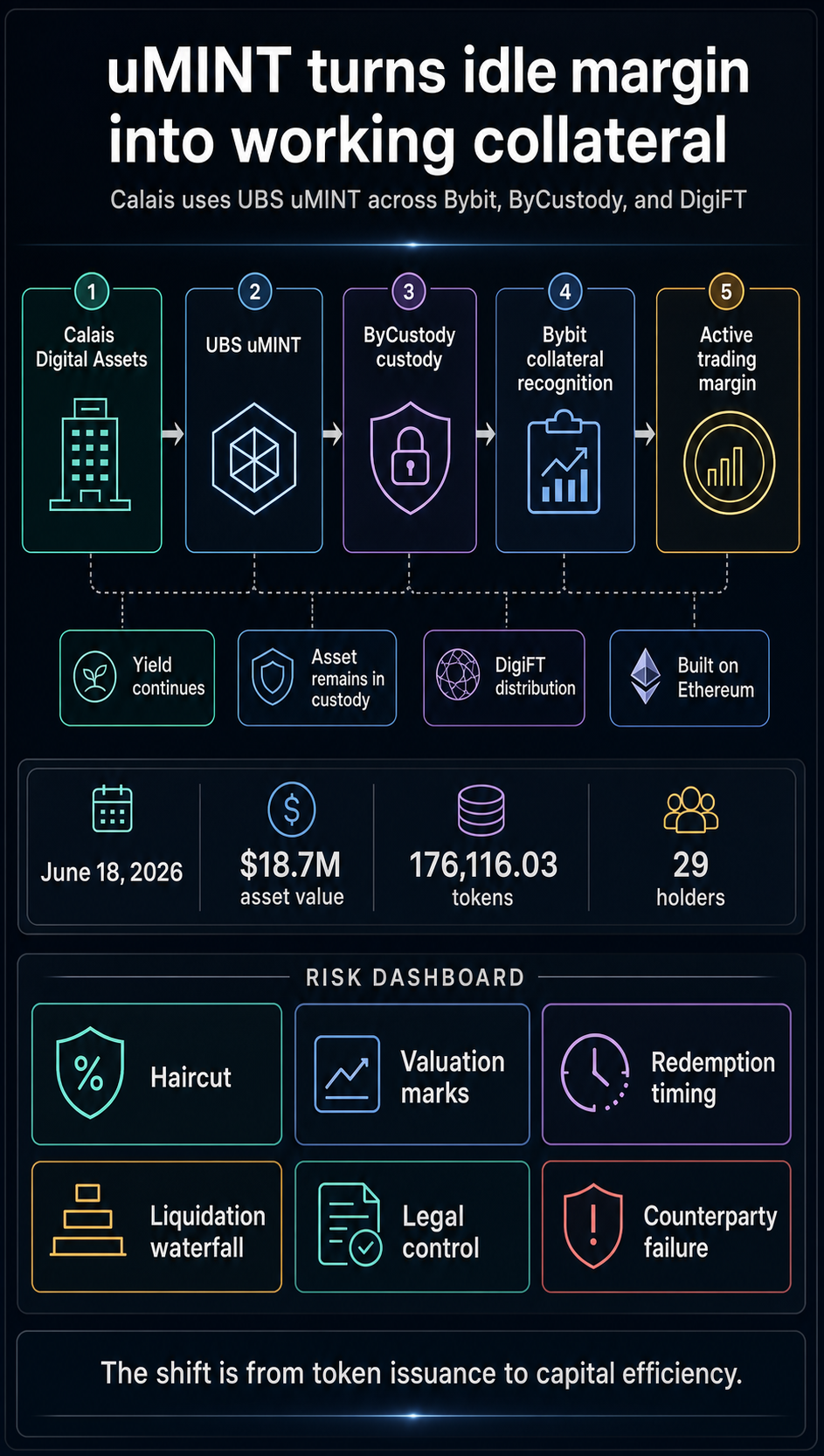

The setup runs across Bybit, ByCustody, and DigiFT, with the uMINT position remaining in custody while it is recognized as exchange collateral.

The June 18 deployment is important because collateral that would typically sit as idle cash or cash equivalent can still earn money-market yield while supporting trading activity.

For tokenized real-world assets, that shifts the discussion from issuance volume to market plumbing. The question is whether these instruments can become useful enough to replace idle margin inside real trading operations.

How UBS uMINT collateral works on Bybit

Calais, a Singapore-headquartered quantitative investment fund, is using UBS uMINT as off-exchange settlement collateral in active trading operations.

The off-exchange settlement collateral transaction runs through a three-party setup: DigiFT provides regulated access and distribution for uMINT, ByCustody holds the asset, and Bybit accepts the custodied position as collateral on its exchange infrastructure.

That changes the economics of margin. Traditional collateral arrangements often require a trader to park cash, stablecoins, or other eligible assets in a form that protects the trading venue while limiting what the fund can earn on those assets.

In DigiFT’s description, Calais can keep exposure to a money-market product while using that same position to support trading.

The distinction is operational rather than cosmetic. A tokenized fund that exists on-chain is useful as a settlement asset only if venues, custodians, distributors, and legal structures agree on how it can be held, valued, and controlled.

A tokenized fund that can also satisfy exchange collateral requirements starts to behave more like a working balance-sheet tool.

| Question | Traditional idle margin | uMINT as OES collateral |

|---|---|---|

| Where the asset sits | Usually posted or reserved for the trading venue | DigiFT says Calais’s uMINT remains in ByCustody |

| Yield treatment | Cash or cash equivalents may stop earning for the trader | DigiFT says Calais maintains yield while trading |

| Exchange utility | Collateral backs trading directly | Bybit recognizes the custodied uMINT as trading collateral |

| Remaining risk | Venue, custody, and margin terms remain central | Haircuts, redemptions, liquidation rights, and legal treatment remain key questions |

The comparison is the core capital-efficiency claim. The tokenized position can be recognized by an exchange while remaining within a custody arrangement designed for institutional use.

That is where the deployment reaches beyond another RWA announcement and becomes a live test of RWA collateral inside exchange margin infrastructure.

It also shows why token issuance alone is only the first layer. The trade requires a distributor, custodian, and exchange to agree on custody, recognition, and operational control before the fund position can function as collateral in practice.

The rails and the scale

The Calais deployment follows earlier plumbing. In October 2025, Bybit, DigiFT, and UBS uMINT introduced institutional access to collateral for the tokenized fund.

That earlier announcement established the basic institutional pitch: shares of UBS’s tokenized money-market fund, distributed through DigiFT, could be used as collateral on Bybit.

In November 2024, uMINT launched as UBS’s first tokenized investment fund. UBS described the UBS USD Money Market Investment Fund Token as a money-market investment built on Ethereum distributed ledger technology.

The product is designed to give tokenholders access to institutional-grade cash management backed by high-quality money-market instruments.

Those details are central because uMINT is being positioned as a conservative cash-management exposure rather than a volatile crypto margin exposure.

The Calais use case is about capital efficiency: a fund wants collateral that remains suitable for trading operations while still staying productive on the balance sheet.

CryptoSlate has already covered the original uMINT launch and the broader trend toward tokenized income products becoming more than passive holdings.

The new step is the specific exchange-margin workflow. The live peg is that an institutional trading client is now using the fund token as recognized collateral inside a Bybit, ByCustody, and DigiFT stack.

The current scale of uMINT still argues for restraint. The uMINT asset page identifies UBS USD Money Market Investment Fund Token as a U.S. Treasury asset on UBS Tokenize, with UBS Asset Management (Singapore) Ltd. as manager and Ethereum as the native ERC-20 network.

On June 21, the total asset value was around $18.7 million, 176,116 tokens, and 29 holders.

Those numbers make the product live but early. They show a real tokenized money-market product with visible on-chain scale wired into an institutional collateral workflow, while broad adoption and standardization across crypto venues remain to be seen.

The scale is small enough to treat the deployment as a test, but the structure is important enough to watch. The question is whether this becomes a repeatable collateral model or remains a bespoke institutional arrangement.

The business issue sits in market structure, rather than price action. CryptoSlate’s aggregate market pages can provide broad context for the size of the crypto market, but the operational driver is whether tokenized funds can be made useful inside repeatable trading processes.

Those processes include custody, collateral recognition, settlement, valuation, liquidity, and risk control.

If the model spreads, the impact would be practical. Funds would have a stronger path to hold yield-bearing cash-management products while posting trading collateral.

Exchanges could compete on the quality of the assets they recognize as margin, as well as on liquidity and fees. Custodians and distributors would become part of the trading stack, rather than only post-trade infrastructure.

The hard questions are still in the margin terms

The same features that make the Calais setup interesting also leave several unresolved questions. Public details released for the deployment omit the haircut Bybit applies to tokenized money-market fund collateral, the valuation source, the frequency of collateral marks, and the liquidation waterfall if losses outpace redemption or transfer processes.

Liquidity timing is another pressure point. Money-market funds are designed for cash-management stability, but they can behave differently from stablecoins during a fast exchange-stress event.

RWA.xyz’s product page lists subscription and redemption fields, while trading firms still need to understand what happens when margin calls, exchange risk systems, and fund liquidity windows collide.

Legal treatment is equally important. Segregated custody can reduce one class of venue risk, while bankruptcy, control, and enforceability questions remain across a multi-party stack.

A fund using the structure still needs confidence about who can move collateral, under what conditions, and what happens if the exchange, custodian, distributor, or another intermediary fails.

Eligibility will also shape adoption. DigiFT’s materials state that the product and services are available only through authorized and regulated intermediaries to eligible investors.

That points to a professional and institutional lane before any use of retail margin. If the model expands, it will likely do so first through qualified clients, approved custodians, and venue-specific collateral rules.

The Calais deployment is best read as a first-client implementation with meaningful implications. It shows a concrete path from token issuance to trading utility: a UBS money-market token distributed through DigiFT can sit in ByCustody and still count as collateral on Bybit.

The deployment reaches a pain point institutions understand. Idle margin is expensive. Yield-bearing collateral is attractive.

But the model only becomes durable if the operational controls can survive the moments when collateral is most important: market volatility, forced deleveraging, liquidity stress, and counterparty failure.

The next test is transparency. More funds and venues may follow, but adoption will depend on whether participants can see the haircut, valuation, redemption, custody, and liquidation rules before volatility tests the stack. Until then, Calais has proved that tokenized money-market collateral can reach live exchange infrastructure. It has yet to prove that the model can scale under stress.