Goldfinch, a crypto lending platform that connected investor capital with real-world borrowers, is now showing what happens after the lending boom ends: the hard risk sits in collecting from borrowers once growth has slowed.

The June 12 GIP-87 proposal would stop new protocol development, wind down Goldfinch Prime, keep legacy app access available, create a U.S. trust structure, and pay Warbler Labs $150,000 USDC for wind-down services.

The proposal remains under governance consideration, with community discussion continuing through June 20. No formal approval or rejection has been publicly recorded at the time of writing. The broader market implication remains the same: tokenized private credit can shift from yield generation to borrower workouts while underlying loans remain active.

In Goldfinch’s case, the next phase centers on recoveries from legacy borrowers, borrower-pool performance issues, servicing costs, and the time it takes to turn loan claims back into cash.

That shift turns DeFi private credit from an access-and-yield pitch into a workout test. For investors, protocols, and RWA lenders, the key question is whether underwriting, default management, and borrower recovery can hold up once the loan book stops growing.

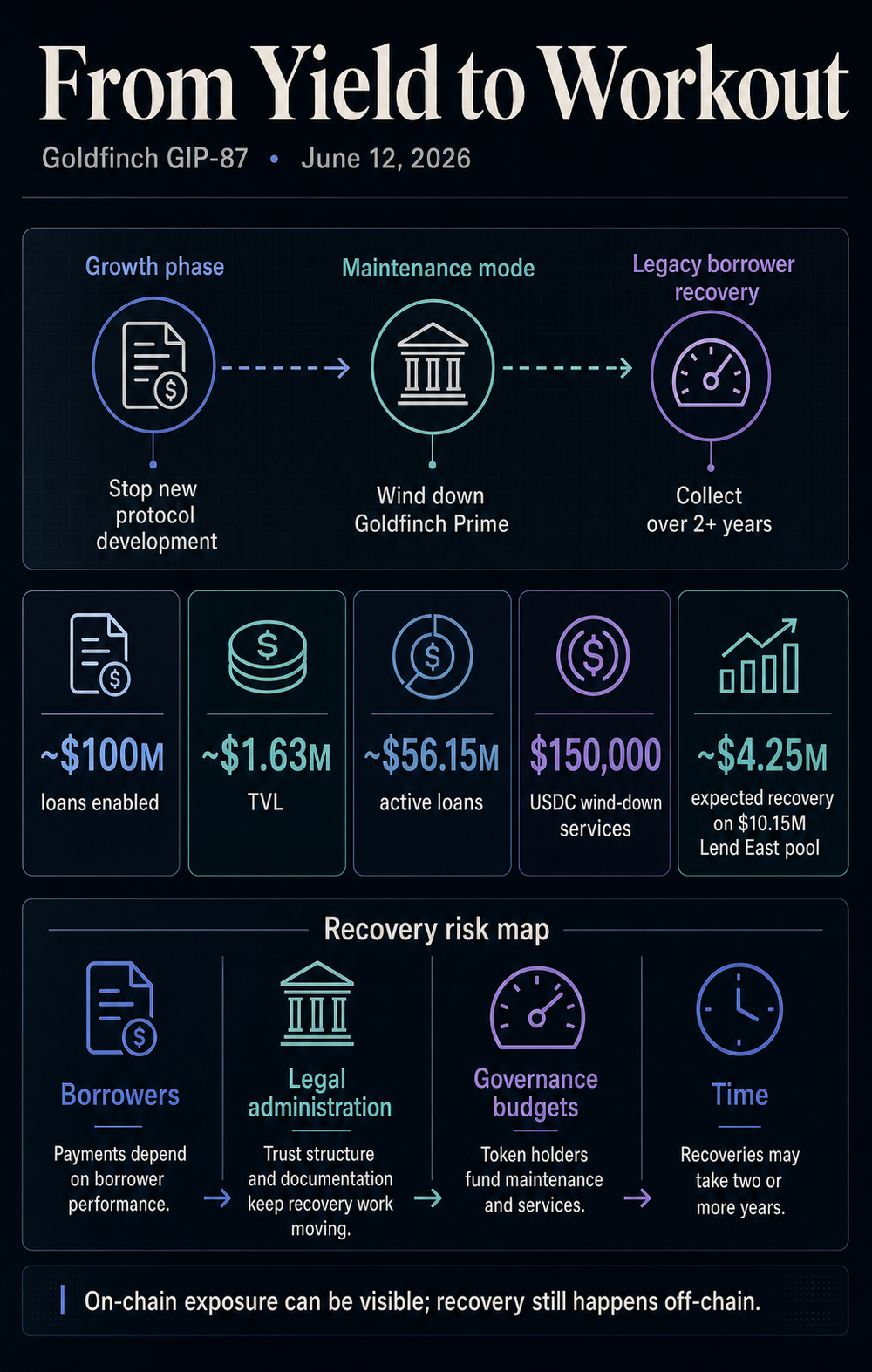

From loan growth to recovery work

The proposal says Goldfinch’s original protocol enabled roughly $100 million in loans, while several borrower pools had serious performance issues. It would put the protocol into maintenance mode rather than fund new development, with operations focused on collecting payments from legacy borrowers.

That is a different business from origination. New lending rewards speed, distribution, and capital formation. Recovery rewards documentation, patience, legal leverage, borrower follow-up, and controls around who pays for the work.

Goldfinch is moving toward a public recovery vehicle for a private-credit book.

Recent public data shows Goldfinch with roughly $1.65 million in TVL, while active loans remain materially larger. The exact figures fluctuate over time, but the key observation remains that the protocol’s active credit exposure significantly exceeds its current on-chain liquidity footprint.

Active loans are excluded from TVL by default, so the two figures describe different aspects of the same problem. TVL can show a small, live DeFi footprint, while active loans show a larger book that still needs to be monitored, serviced, or recovered.

| Metric or term | Growth-era reading | Workout-era reading |

|---|---|---|

| About $100 million in loans enabled | Evidence that Goldfinch reached meaningful private-credit scale | A larger recovery surface if borrower performance deteriorates |

| About $1.63 million in TVL on June 23 | A small current DeFi liquidity footprint | Limited on-chain capital relative to the work still attached to active loans |

| About $56.15 million in active loans on June 23 | Evidence that the loan book has residual exposure | A reminder that exposure can outlast growth capital and token momentum |

| $150,000 USDC wind-down services payment | A governance budget line | A visible cost of servicing and recovery after origination |

| About $4.25 million expected recovery on a $10.15 million Lend East pool in April 2024 | A borrower-pool update | A concrete example of how private-credit losses can become slow recovery math |

Public lending dashboards continue to show a large gap between Goldfinch’s TVL and its active-loan book. Those metrics capture different parts of the system.

TVL reflects capital currently parked in the protocol, while active loans represent credit exposure that still requires servicing, monitoring, restructuring, or recovery. The persistence of that gap highlights how recovery obligations can outlast a protocol’s growth phase.

That gap is where tokenized private credit begins to look less like liquid DeFi and more like a public wrapper around private-credit servicing.

The risk disclosures point in the same direction. Senior Pool documentation warned that participants could lose money if borrowers failed to repay and could face liquidity limits if there was insufficient USDC in the pool.

The wind-down turns those general product risks into governance logistics: how much should still be funded, who performs the work, how legacy users retain access to the app, and what legal structure handles borrower recovery.

The Lend East borrower update gives those questions a concrete shape. In April 2024, a Goldfinch forum update said the pool was expected to repay about $4.25 million against a $10.15 million Goldfinch pool at that time, implying a large expected principal shortfall.

That was an expected recovery figure at the time of the update, before any final realized outcome. It still shows how private-credit recovery becomes a matter of timelines, shortfalls, negotiations, and legal paths rather than dashboard balances.

That is where DeFi private credit collides with traditional private credit. Blockchains can make positions, tokens, and protocol activity easier to observe. Actual repayment still depends on borrower behavior, servicing, documentation, and legal paths when a loan goes wrong.

Governance becomes part of the credit stack

The $150,000 USDC payment to Warbler Labs is small compared with Goldfinch’s historical loan origination, but it makes the recovery function explicit. In a growth phase, governance budgets often fund development, incentives, integrations, or expansion.

In the wind-down phase, the budget covers maintenance, app continuity, legal administration, and the labor required to collect on existing obligations.

That changes what token holders are voting on. The decision concerns how a credit book should be serviced after growth capital has exited.

The proposal’s U.S. trust structure and continued legacy app access point to a phase in which the system must preserve sufficient infrastructure for payments and recoveries while scaling back work unrelated to the old loan book.

For RWA lenders, the lesson is an uncomfortable one. A tokenized private-credit platform has to prove more than origination demand. It has to prove borrower selection, reporting discipline, recovery administration, servicing incentives, and governance controls.

If those pieces are weak, the chain can make the damage visible without making the recovery easy.

Recent CryptoSlate coverage has shown the growth side of the same market. One private-credit lender is trying to use AI to compress months of paperwork into one-day on-chain loans, while broader RWA coverage has focused on how tokenized assets fit into DeFi’s composability limits.

Goldfinch’s proposal adds the part that expansion narratives leave for later. Faster origination must be paired with a credible process for handling slow repayment, missed payments, and disputes.

That contrast also explains why Goldfinch should be read carefully. The proposal is a live example of how the credit stack changes after the origination phase, with demand elsewhere in RWA lending still greater than this single case.

The assets may be represented on-chain, but the recovery process still runs through borrower behavior, legal administration, documentation, and governance-funded work.

What RWA lenders have to prove next

Goldfinch is one specific case in tokenized private credit. DefiLlama data still shows broader RWA lending TVL and DeFi active-loan activity well beyond Goldfinch’s current footprint, leaving the sector’s demand picture larger than one protocol’s maintenance-mode proposal.

The more useful takeaway is specific. Tokenized private credit has two markets at once. One appears when capital is deployed, yields are discussed, and token prices trade.

The other appears later, when borrowers miss targets, recovery takes years, and governance has to decide whether to keep paying for the machinery that collects the remaining cash.

That makes Goldfinch as much a recovery trade as a DeFi protocol. Its future value depends less on new protocol features and more on borrower payments, recovery administration, and whether the proposed structure can preserve enough operational capacity to collect what remains.

The next signals are practical. A formal governance outcome would clarify whether GIP-87 becomes the operating path. Updates from the proposed trust or administrators would show whether recovery work has a clear cadence.

Borrower payment updates would show whether the active-loan footprint converts into cash or remains stuck in negotiation. Other RWA lenders will also have to show how they disclose borrower performance, fund servicing work, and protect users when private-credit loans stop behaving like yield products.

Goldfinch’s answer to the recovery-risk question is blunt. On-chain private credit can make exposure easier to track, but recovery still depends on off-chain borrowers, legal administration, governance budgets, and time.

The yield pitch brings capital in. The workout tests whether the credit was sound.